Monday 12 Dec 2022, 00:01

Mortgage lending to fall 15 per cent next year, returning to pre-pandemic levels.

UK Finance has today published its mortgage market forecast for 2023 – 2024, anticipating a softening in the mortgage market next year that marks a return to pre-pandemic norms.

Key points for 2023:

- Overall mortgage lending is expected to fall 15 per cent, a return to pre-pandemic levels.

- Lending for house purchase mortgages is predicted to fall 23 per cent due to cost-of-living pressures and rising interest rates placing pressure on affordability. New lending to buy-to-let landlords is predicted to fall 27 per cent in 2023.

- Property transactions are predicted to fall by 21 per cent next year.

- Refinancing will increase with strong numbers of fixed rate deals due to end in 2023.

- If a customer is struggling with their payments, lenders will assess a borrower’s financial circumstances and offer a form of forbearance tailored to their individual circumstances.

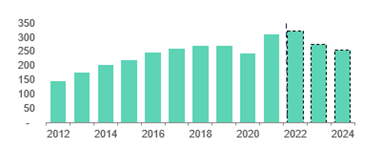

Amid challenging times for the UK economy, we expect cost of living pressures and rising interest rates to reduce demand for house purchases between 2023 - 2024.

We expect the number of property transactions to fall 21 per cent next year (from around 1.2 million in 2022 to 1 million in 2023), with the value of lending to homeowners dropping 23 per cent, and lending to landlords falling 27 per cent. Despite the anticipated fall in activity, the UK has a strong mortgage and housing market which will remain competitive.

At the same time, we expect to see strong demand for refinancing as around 1.8 million fixed rate mortgage deals are scheduled to end in 2023.

Affordability pressures facing borrowers will mean some borrowers, particularly amongst lower income brackets, may find remortgaging options more limited on the open market. However, with widespread availability of internal product transfers, we expect refinancing overall to be strong through next year. We expect to see around £212 billion of product transfers to take place next year, compared with an estimated £197 billion in 2022.

Chart 1: Gross mortgage lending, £ billions

Arrears to rise gradually from historic lows

With forecasts for unemployment showing a relatively small increase, we expect the vast majority of borrowers will be able to maintain their mortgage payments.

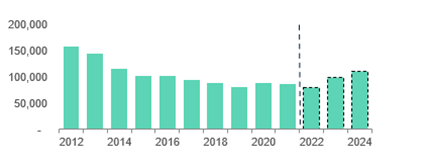

However, any rise in unemployment, coupled with cost of living pressures and interest rate increases, will put further pressure on some households. We expect this pressure will begin to show in rising mortgage arrears from early 2023, increasing through the year and into 2024. We anticipate the number of households in arrears to reach 98,500 next year, representing around one per cent of outstanding mortgages. By historic standards these increases arrears figures do remain low.

Possessions numbers rose modestly during 2022 as lenders and the courts worked through the backlog of cases that had built up due to the pandemic induced possessions moratoriums. As historic cases make their way through the courts the number of possession cases has risen and we expect this to continue slowly through the next two years as the backlog is cleared. However, as noted above with arrears the increase in the number of properties being repossessed remains low compared to the years prior to the Covid-19 pandemic.

However, with arrears currently still low and with few new arrears cases emerging to date, we do not expect material numbers of possessions related either Covid-19 or the current headwinds facing household finances until well into 2024.

It is important to note that possession is only ever a last resort and taken when all other forms of support have been explored with the borrower. Support is available to all customers who might be struggling with their mortgage payments. We would encourage borrowers to get in touch with their lender early to discuss the tailored options available for their particular circumstances.

Chart 2: 1st charge mortgage arrears

James Tatch, Principal, Data and Research at UK Finance, said:

"As we look ahead, the mortgage market is expected to enter a period of relative weakness from next year as house prices, the cost-of-living and interest rate pressures put a brake on new demand.

“The high level of activity during the 2021 Stamp Duty holiday means that a large number of borrowers are due to refinance next year, pushing up the expected value of refinancing in 2023. The pressures being seen on household finances could mean that some customers have fewer options. However, there is wide availability of product transfers - we would encourage customers to speak to a whole of market mortgage adviser to discuss the options best suited to their circumstances.

"As always, any customers who find themselves in difficulty should speak to their lender at an early stage, as the industry stands ready to help with a range of forbearance options that can be tailored to best suit individual customers' circumstances."

Contact Information

UK Finance Press Office

020 7416 6750

press@ukfinance.org.uk

Notes to editors

For more information call the UK Finance press office on 0207416 6750 or email at press@ukfinance.org.uk.

- UK Finance is the collective voice for the banking and finance industry. Representing more than 300 firms across the industry, we act to enhance competitiveness, support customers and facilitate innovation.

- You can access the mortgage market forecast in full here.

- The banking industry has increased funding for free debt advice across the UK to £99 million.

- UK Finance has published guidance on support for customers in payment difficulties here.

- If a customer is struggling with their payments, lenders will assess a borrower’s financial circumstances and offer a form of forbearance tailored to their individual circumstances. This could include:

- Part payment plans

- A mortgage term extension

- Temporary switch to interest-only

- Payment concession, including a zero-payment concession if appropriate.

- In the November 2022 autumn statement, the government announced that mortgage customers in financial difficulty will have earlier access to its Support for Mortgage Interest scheme, and the ‘zero-earnings’ rule will be removed.

About Us

For more information please call the UK Finance press office on 020 7416 6750 or email press@ukfinance.org.uk

Representing 300 firms, we’re a centre of trust, expertise and collaboration at the heart of financial services. Championing a thriving sector and building a better society.

Powered by Onclusive PR Manager © 2026