Monday 4 Mar 2024, 10:00

Affordability pressures push down mortgage lending and savings in 2023

UK Finance today releases its latest Household Finance Review for Q4 2023, exploring trends across household, spending, saving, and borrowing.

- Affordability pressures led to a weak mortgage market in 2023. The same pressures are likely to hold back activity in 2024, although forward data suggests some recovery in the first quarter.

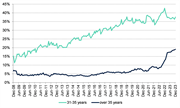

- One in five first-time buyers (FTBs) borrowed for a term of more than 35 years, compared to fewer than one in ten the year before, as a means of improving their affordability position.

- Despite this, FTBs continued to face significant affordability challenges in 2023 with the number of loans to this group falling to their lowest level since 2013.

- Meanwhile, savings levels fell each month last year, for the first time in 25 years, as households raided their rainy-day funds to cover higher bills and expenditure. But many households, particularly those without savings, will have needed to make cuts to their monthly spend.

Mortgage lending

Over the whole of 2023, the increased cost of living, coupled with higher mortgage interest rates, led to a sharp fall in mortgage lending across all sectors.

The number of loans made to FTBs last year was the lowest since 2013, down 22.4 per cent on 2022. But home movers, most of whom do not receive the same sort of help from family support or Stamp Duty exemptions, were hit even harder, with loan numbers falling by 26 per cent. The 251,000 loans to home movers last year was the lowest figure since 1974.

For households who bought a home last year, affordability pressures meant borrowers were choosing longer mortgage terms to lower the cost of monthly payments. By the end of 2023, almost one in five FTBs were borrowing with a term of over 35 years, compared with fewer than one in ten the year before.

However, more positively, the number of applications for mortgage loans rose in Q4 2023. With inflation pressures easing, and expectations of lower borrowing costs to follow, the rise in applications signals that the market could grow in early 2024.

Proportion of new FTB mortgages taken out with over 30-year term

Source: UK Finance

Consumer spending and borrowing

Inflation is currently on a downward path, but price increases last year did impact spending. Although higher prices pushed up the value of consumer spending last year, UK Finance data shows that growth in the number of sales slowed at the end of last year – with spending on non-essential items especially weak. Many households, particularly those who do not have a cushion of savings which they can now draw on, are having to cut back on spending where their income can no longer cover everything it did previously.

Despite the continuing cost of living pressures, households are managing unsecured debt well. Overdraft debt continued its downward trend, and half of all credit card balances were interest-bearing, which is the lowest proportion since 1995 when UK Finance records began. Personal loan borrowing also fell away in Q4 in line with seasonal trends.

However, lasting cost of living pressures led to the total level of personal savings falling each month in 2023. This is something that has not been seen for at least 25 years.

Change in household deposit levels

Source: UK Finance

Mortgage arrears and support

Mortgages in arrears rose throughout 2023 to 107,250. This number still accounts for less than one per cent of the total number of outstanding mortgages. The figure suggests that the Financial Conduct Authority-mandated stress tests, which ensure borrowers can cope with higher interest rates, continue to work effectively to keep recent borrowers out of payment difficulties. As previously announced, we do expect arrears cases to increase in 2024, but not at the same pace as in 2023.

The number of possessions remained largely static during 2023, numbering 1,150 in Q4 and 4,620 in 2023 as a whole. The possessions that are taking place are long-term cases from before the pandemic.

Eric Leenders, Managing Director of Personal Finance at UK Finance, said, “2023 was a tough year for UK households and we expect to see continued challenges in 2024. Affordability remains a barrier to home ownership, but pressures should start to ease gradually through this year and next.

“Amidst ongoing cost challenges, it’s encouraging that customers don’t look to be running up higher levels of unsecured debt. But we know some households will be more affected than others - if you are struggling with personal loan, credit card or mortgage repayments, please reach out to your lender as soon as possible for help.”

Contact Information

UK Finance Press Office

020 7416 6750

press@ukfinance.org.uk

Notes to editors

- UK Finance classifies mortgages as being in arrears when the arrears reach 2.5 per cent of the outstanding balance

- More information on the support available for mortgage customers can be seen via the banking industry’s Reach Out campaign here

- More information on the Mortgage Charter can be seen here

About Us

For more information please call the UK Finance press office on 020 7416 6750 or email press@ukfinance.org.uk

Representing 300 firms, we’re a centre of trust, expertise and collaboration at the heart of financial services. Championing a thriving sector and building a better society.

Powered by Onclusive PR Manager © 2026